As we move through March 2026, the connection between personal banking and business payroll has changed significantly. People over 67 now need to engage actively with their employer and the bank’s security AI to keep track of their money effectively.

The Fair Work Agency (FWA) formally opened on April 7, 2026, making HMRC’s digital enforcement triggers tougher. Because of this, the financial culture has shifted toward “check and verify.” This guide shows how to navigate these automated limits so that your data remains safe while ensuring convenient access to your pension and funds.

Why Are These Limits Changing?

The UK’s financial system has reached a stage where it must find a balance between being safe for elderly people and being digitally efficient. The government and banks have set up a “tripwire” mechanism that activates when certain transaction patterns or amounts, often centered around £500, occur in a bank account.

For persons over 67, these limits are part of a larger safety net that includes the FWA and new HMRC debt recovery protocols. It is easier for the system to flag suspicious activity when there is a soft restriction of £500, allowing retirees and employers to “take a second look” before significant funds are moved.

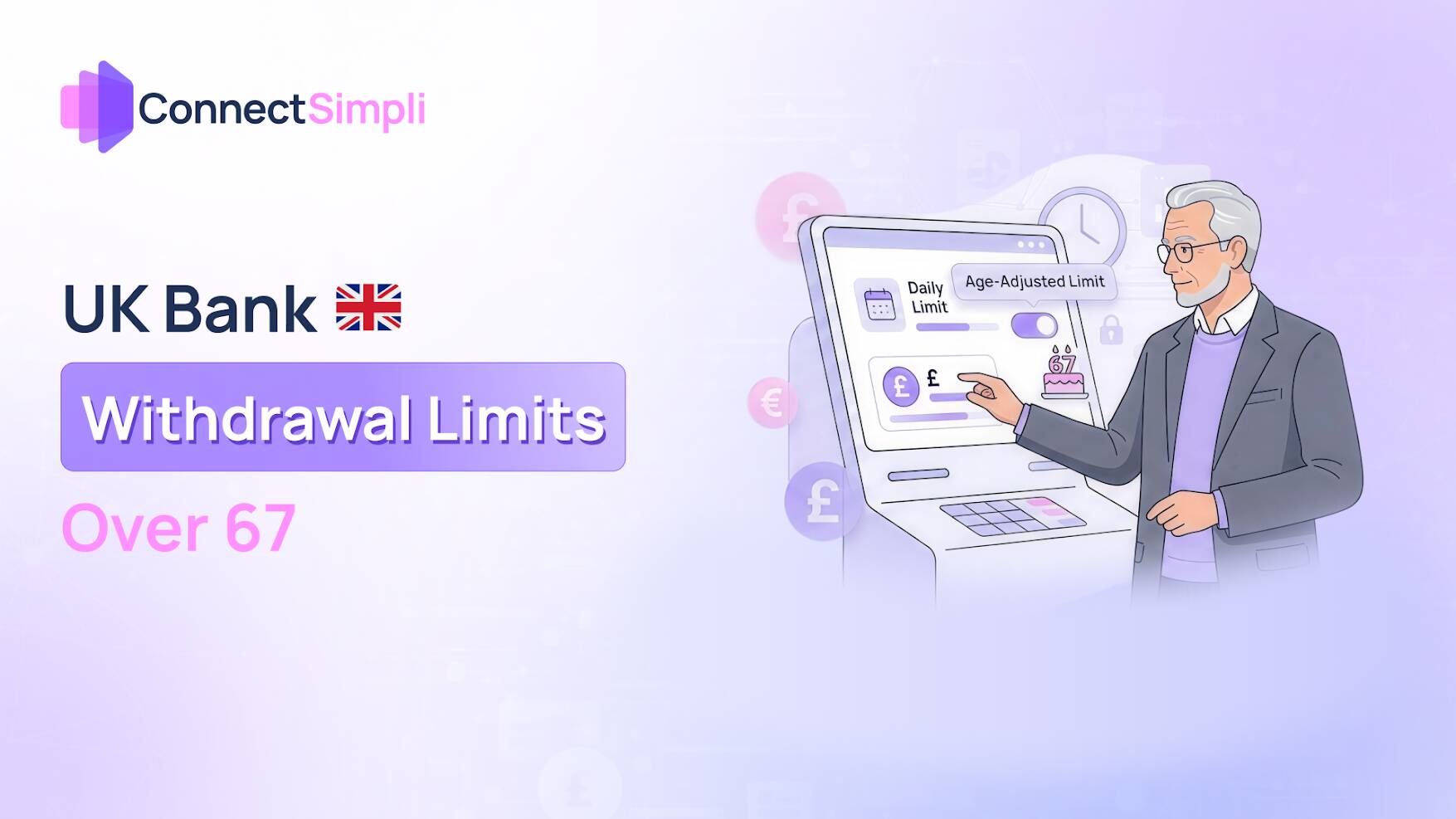

The New Reality of Withdrawal Limits for Retirees

- The Daily ATM Standard of £500: Most current accounts in the UK, including those from Starling, Nationwide, and HSBC, now set a £500 daily ATM restriction for people over 60 to prevent rapid cash draining by fraudsters.

- The Safe Withdrawal Methodology: Bank counter workers must now follow a verification methodology for cash needs over £2,000. This includes asking simple, quick questions to ensure the withdrawal isn’t part of a scam.

- Pre-Authorization through Banking Apps: People can bypass default limits by using Pre-Authorization. If you notify a bank 24 hours in advance through an official banking app, you can temporarily loosen limits without a permanent security freeze.

The Employer’s Perspective: Funding the Pension Pot

- Dealing with Business Bank Limits: Starting in April 2026, the New State Pension will rise to £241.30 a week. Corporate accounts need greater daily transfer limits to avoid rejection of bulk pension payments.

- The Pre-Payment Audit: Payroll administrators now verify their bank’s single transaction daily value limits before every run. This prevents automated security systems from “throttling” transfers of large amounts.

- Corporate Communication: HR departments are essential for clarifying that “held funds” are often a security feature of 2026 AI on the bank side, rather than a mistake in the payroll software.

Payroll & HR Software Integration

- Protocols for Maker-Checker 2.0: Modern software like Connect Simpli now alert users to every manual pension change over £500 for a second approval. The FWA mandates a “Maker” to submit data and a “Checker” (manager) to approve it.

- Fair Work Agency Enforcement: Strictly enforcing the National Minimum Wage and Statutory Sick Pay, the FWA can penalize employers up to 200% of the difference for payment errors.

- Direct Bank Integration: Systems now use Faster Payments to ensure money reaches retirees’ accounts on schedule, even when personal security holds are in place in other sections of the system.

Critical Compliance Concerns

- The £5,000 Safety Buffer: HMRC’s Direct Recovery of Debt (DRD) cannot take money from a retiree if it leaves them with less than £5,000 in their combined accounts.

- Simple Assessment (PA302) Alerts: A sudden £500 drop in take-home pension is generally an automated Simple Assessment collection for taxes linked to the frozen £12,570 Personal Allowance.

- Fraud Alert: Your bank or HMRC would never text or email to ask for a “£500 fee” to raise your withdrawal limit or release a pension payment.

Management’s Strategic Checklist

- Limit Verification: Check the company’s withdrawal caps against its overall pension liabilities once a month.

- Exception Reporting: Use reporting tools to locate employees whose net pay could set off a security flag or an FWA audit.

- Staff Education: Teach line managers to explain Fiscal Drag and the 10.75% Dividend Tax so employees over 67 understand why tax laws have changed.

Conclusion:

The banking and payroll world of 2026 is founded on transparency and investigation. Whether it is a retiree checking an official app for a limit increase or a manager approving a £500 change, the goal remains the same: ensuring financial security through enhanced communication. As long as both sides stick to the £5,000 safety buffer and employ Maker-Checker software, they can feel safe heading into the new tax year.

VI. Frequently Asked Questions (FAQ)

Q: Why did HMRC take £500 from my bank account without a court order?

A: Under Direct Recovery of Debt, HMRC can collect unpaid taxes directly if you ignore contact. They must legally leave at least £5,000 in your account.

Q: Can I change the £500 limit on my ATM?

A: Yes. It is a bank setting, not a legal cap. You can increase this via your mobile banking app or at a branch. It is better to do this 24 hours ahead of time.

Q: How can I tell whether a £500 deduction is wrong?

A: Check your Personal Tax Account first. If there is no record, call your bank’s fraud department straight away.

Q: What should I do if a letter from HMRC seems fishy?

A: Consult the official GOV.UK “Check if it’s genuine” list. HMRC never asks for a “release fee” via SMS or email.